How I Optimized My Retirement Saving in Year 1 in Tech

How I Optimized My Retirement Saving in Year 1 in Tech

Time in the Market > Timing the Market

Disclaimer: I am not a financial advisor, accountant or tax expert, nor do I claim to be. The information in this post is not a substitute for financial advice from a professional who is aware of the facts and circumstances of your individual situation. This is purely my own experience trying to learn personal finance and build a better future.

In the personal finance space, there is a lot of very sound advice about how to get started saving and how to prioritize. Two great examples are Dave Ramsey’s Baby Steps and the Money Guy’s Financial Order of Operations. Personally, I prefer the latter because it’s aggressive (shoutout to the financial mutants). Still, they come back to earth and stay realistic relative to the current market (like on housing down payments).

What you don’t see a lot of are good examples, and as someone who likes to pick apart case studies and visualize what success looks like, that bothers me. So, today I thought I would share an example of how a real person starts to save for retirement working in technology.

While I’ve done my best to be responsible, I am in no way claiming this is the only way or the best way to kick off your saving journey. I simply find anecdotes relatable and wish I could find more resources on how someone in my situation thinks about retirement. So if you’re like me, I hope you find this useful. Here are the primary steps I honed in on that set me up for success.

Set up 401k

Hone in budget

Take advantage of lower income and underperforming funny money

Waiting until the tax filing deadline

Taking advantage of employer benefits

As I’ve mentioned before, I started full-time in June. That means I only worked for 7/12 months of the year. As a tech employee and recent graduate, that means I was fortunate enough to receive a sign-on bonus and relocation assistance. A significant portion of my compensation is via RSUs - in themselves a big topic to discuss - but the first chunk won’t vest until over a year at the company, so let’s ignore those for now and just focus on the monthly picture.

Set Up 401k

Setting up my 401k investments was extremely easy to start, so I immediately took advantage of the fact that I could simply pick a portion of my income and a simple target-date fund. Now, I have since made many adjustments already, but the main idea is that I set up what I thought was a good goal for saving from the get-go, which was initially 10%. I did not wait for a full paycheck or two and then sign up because man is it hard to go back once you get a taste of that fat paycheck.

Since signing up I’ve revisited my traditional vs Roth decision now that I understand the distinction, I’ve dabbled in having my funds managed, and also reconsidered my contribution amount.

Spoiler Alert

Trad vs Roth: Opting for Roth since I’m young and may have a higher income in the future. Match is always traditional so I’m keeping an eye on the bucket strategy. If I’m lucky, I’ll make enough to consider taking the up-front deduction in due time.

401k Management: Management was interesting to see as far as asset allocation, but I decided against it in favor of the simple, low-cost funds that were available. Fidelity also offers Brokeragelink which I’m considering.

The fees were surprisingly low, but I just don’t see the need if I pay attention to my allocation and adjust with time. They chose the same low-cost funds. Plus, I like to understand it myself instead of flying blind.

Allocation: I’m going to get more aggressive in 2023, more on that later.

Hone in my budget

With a 401k just budding I made it a priority to track my cashflow and identify where I needed to allocate more money and where I could pull back. Once I became more confident in my budget it made it exponentially easier to know how to save for future goals or change my retirement contributions, but with such a sudden change in income that took some time. Please refer back to my previous post for more details on getting started with a Budget.

With the help of the tools available today, saving can even be gamified, and it makes saving feel even more rewarding than buying ourselves the things we don’t really need. Budgeting and tracking your finances are really just clearing out all the unknowns so we can make future progress with confidence.

Take Advantage of Lower Income in Partial Year

Since I started working in the middle of the year, I had a partial year of income, which put me in a lower tax bracket. Instead of my full salary plus bonus and relocation, my salary earnings for the 2022 tax year were quite a bit lower. I took advantage of this by directly contributing to a Roth IRA since I came in under the income limits for direct contributions. Normally I would have to do a backdoor conversion, but this year’s lower earnings allowed me to maximize my retirement savings potential and take advantage of the tax-free growth of a Roth IRA.

Another kicker I was able to implement here was to use the funny money I had been investing in a regular brokerage account for my Roth IRA contributions. My tech-heavy and extremely speculative portfolio that I built over my college years was not performing well, was not diversified, and was frankly not conducive to long-term growth. It was just gambling and speculation. And no, I don’t have GME 😅.

So, since I was thinking about reallocating these assets anyway, I sold my individual stocks and nearly fully funded my Roth IRA where I could build a straightforward but diverse 2 or 3-fund portfolio that would be well-oriented for long-term success.

Take Advantage of Time Until Tax Filing Deadline

Speaking of funding the Roth IRA, even after the end of the tax year, there is still time to make retirement contributions for the previous year. I made sure to take advantage of this by contributing to my Roth IRA for 2022 before the tax filing deadline in April of 2023. There are perhaps more efficient ways to perform this saving technique, but hey we’re just starting out here (though I’d love to hear how I should have done this better).

Since my portfolio was down, I could sell without capital gains (although, paying taxes should be thought of as a good thing since it means you made money). However, by waiting until the 2023 calendar year, I could not take any tax-loss harvesting for 2022 taxes. I chose to wait because it was my first year filing taxes solo and I wanted to consult a professional CPA about my tax situation both this year and in the future (like my RSUs and stuff). I can still claim the losses for 2023, it’s just not as optimal. Then again, I was able to be more confident in my decision on the tax situation and could still fully fund a 2022 Roth IRA, so I’m happy.

Take Advantage of Employee Benefits

While our regular retirement plans are great vehicles for the lion’s share of saving, there are also other methods that deservedly require some attention. For a young, healthy person like myself, the HSA is a fantastic option. In addition to my contributions to the 401k, IRA, and emergency fund, I moved aggressively to fully fund an HSA for 2022.

This required higher contributions per paycheck, ~$600 a month, but the triple tax advantage of HSAs makes it an absolute star for saving. HSAs only allow $3650 for the year, but with those tax savings and employer contributions, the HSA is extremely hard to beat on a per-dollar basis.

My employer had a great series of talks and videos explaining the HSA, and it was really a great fit for me. I have used it for miscellaneous medical expenses to the tune of a couple hundred dollars, but I’m considering stopping with those and paying out of pocket in the future.

I am a bit hamstrung by the HSA program where I work. I can only invest once my balance exceeds $2000 and with Betterment, the only option is to choose your stock/bond split. You don’t get to pick the individual funds, but the choices were solid and low-cost to my eyes.

While I withhold the right to continue to optimize my HSA in the future, it will still function as a fantastic vehicle for retirement planning. And barring any unforeseen circumstances, it’s entirely possible that the first couple of years of building an HSA could cover a year or more of retirement income.

Visualizing

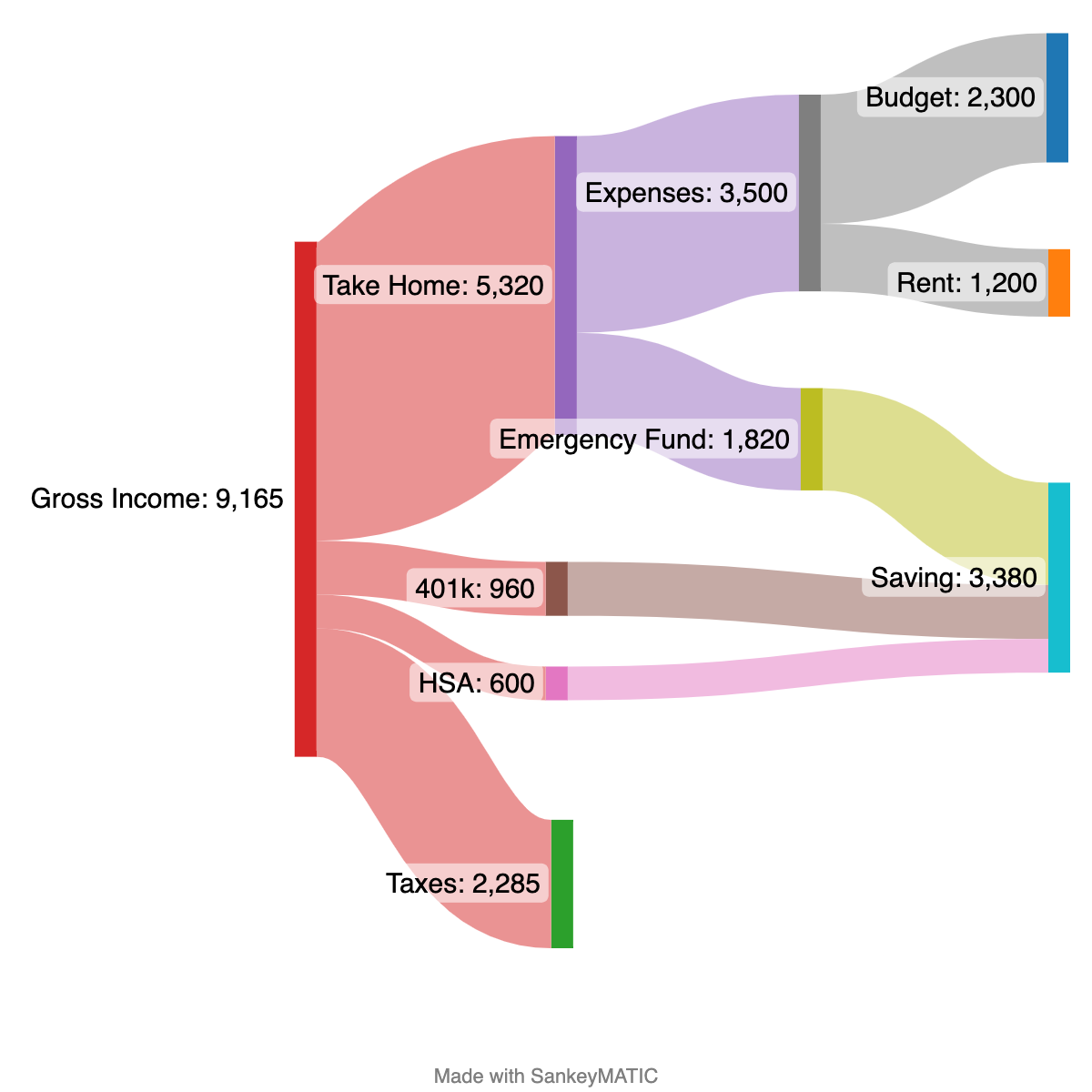

Okay, now that we’ve seen the story in words, what does this allocation look like and how do I plan to adapt it in the future? For this, I like the Sankey Diagram. As you’ll see, they are an attention-grabbing graphical representation of data flows and are perfect for cashflow scenarios.

I think it’s worth mentioning that my salary is quite good (not complaining!), but if you check my position at levels.fyi it’s actually below average and there is room for future wage growth. Still, it’s important to set solid habits early. Any future earnings can go to important saving funds and will only further prepare us for the long haul. What I’m saying is it’s better to prepare now and be happily surprised with extra money in the future. That said, here is a roughly approximated cashflow for 2022.

As you can see, there is a lot that goes into creating a successful saving strategy, but here is a 2-step breakdown from my perspective.

Reasonable costs and expenses

I do not live alone and although we share the rent payment, we split it in proportion to income.

That budgeting thing we talked about. Just be aware of where your money is going, and absolutely make sure you spend less than you make, preferably much less. On the other hand, I have $300 allocated to gifts in my monthly budget. You can be generous to yourself and others, but it must be part of your budget.

My tax math here isn’t perfect, but it’s overestimated when you factor in the standard deduction. This is pretty accurate for my paychecks and I will still receive a tax refund check this year.

Choose saving strategies and start

Choose savings that come out of your paycheck.

Set a lofty 401k goal and pay yourself first.

Contribute to an HSA if it’s the right move for you.

Build that emergency fund.

In the diagram above you’ll see that almost everything extra I brought home went into a high-yield savings account (HYSA) as an emergency fund.

Notice I’m saving almost 37% of my gross income and 63% of my take home. Boy, that’s a good feeling. And I can still live comfortably!

So how do we go from here? This exercise might be helpful for people in their first year, but how does one turn the corner and continue this growth? You’re in luck because I’m already mapping out my 2023 cashflow goals. I haven’t made it to this exact allocation yet, but I’m well on my way to making it a reality.

These are the adjustments I’m making:

With an emergency fund in place, I’m moving towards regular dollar-cost averaging into my Roth IRA via the backdoor and saving the rest for future expenses like a wedding, vacation, or house down payment (where future windfalls will also go).

I’m updating my retirement accounts so I will still be saving the same amount. That means doubling 401k contributions to bring me close to the yearly limit. Luckily, my HSA contributions are down because I’ll have more pay periods to spread that $3650 out over.

I kept taxes the same on this diagram, but they may need some tweaking as my paychecks continue to change. Still, this is an overestimation on the year with the standard deduction.

Now again, these are just rough approximations. 1-time events change the calculus like paying for engagement rings or your big RSU bonus. But with this strategy and continued refining as needed, I can live happily on just my salary. Anything extra coming down the road can be considered additional savings for big events, not something I’m counting on for monthly payments.

I’m looking forward to making this happen this year and revisiting this post and my net worth next winter. Hope you can join me!